ETF投資,美股投資,臺股ETF投資,西洋情歌,西洋音樂,閱讀與興趣 [ラブソング, песня любви][ETF inversión, ETF投資します, ETF инвестиции], all investment and interesting stuff I touched, experienced;

Truckload tender volumes (OTVI) remain the weakest of the three major demand-side indicators in SONAR. In contrast, loaded inter-modal containers moving by rail (ORAILL) are averaging more than a 7% year-over-year increase, and container import bookings (IOTI) are showing similar gains after clearing the Lunar New Year period.

The takeaway: The freight market remains in a holding pattern, while financial markets struggle to interpret what seems to be an ongoing trade policy standoff. 重點:貨運市場仍處於等待狀態,而金融市場則難以解讀似乎持續的貿易政策僵局。

At the time of writing – a caveat now necessary in any discussion involving tariffs due to the pace of change – tariffs on Chinese goods have climbed to 125%, placing immense pressure on businesses that source products from China. 在撰寫本文時——由於變化速度太快,任何涉及關稅的討論都需要提出警告——中國商品的關稅已攀升至 125%,這給從中國採購產品的企業帶來了巨大壓力。

China remains the dominant origin for containerized goods entering the U.S. by sea. Many companies began diversifying their supply chains away from China following the COVID pandemic, which exposed the risks of over-dependence on Chinese manufacturing. Some of this shift began during the Trump administration as trade tensions intensified.

This most recent wave of tariffs and negotiations has left many supply chain managers in limbo. Many had expected more time and clearer guidance to move production to countries like Mexico and Vietnam. Instead, a series of blanket tariffs – including early measures targeting North American trade partners – has left them uncertain about their next steps.

Meanwhile, truckload demand has dropped nearly 10% over the past year, as shippers increasingly turn to inter-modal solutions for domestic transportation. 同時,由於托運人越來越多地轉向多式聯運解決方案進行國內運輸,卡車運輸需求在過去一年中下降了近 10%。

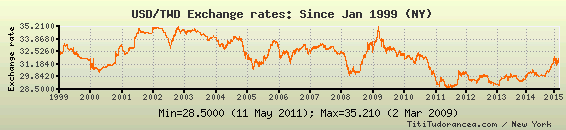

美國的海運和陸運數據正在下降,這一趨勢對經濟造成了負面影響,主要是由於關稅政策引發的進口成本上升和市場不確定性。在當前的貿易戰背景下,中美貿易量減少的情況下,美元走弱和美國公債利率升高的現象可以從以下幾個方面來解釋:U.S. sea and land transport data are declining, a trend that has had a negative impact on the economy, mainly due to rising import costs and market uncertainty caused by tariff policies. In the context of the current trade war, the weakening of the US dollar and the rise in US Treasury bond yields can be explained in the following ways:

總體來看,美國的海運和陸運數據下降反映了經濟活動的減少,這對供應鏈、消費者行為和整體經濟增長都可能產生深遠的影響,台灣則注意長榮、陽明海運。Overall, the decline in U.S. sea and land transportation data reflects a reduction in economic activity, which could have far-reaching implications for supply chains, consumer behavior, and overall economic growth.

根據最新的資訊,2025年美國公債到期的情況及川普關稅政策對經濟風險的影響如下:According to the latest information, the maturity of U.S. Treasury bonds in 2025 and the impact of Trump’s tariff policy on economic risks are as follows:

在2025年,美國將面臨大量的公債到期,預計到期的國債總額約為9.2兆美元,這些到期的債務主要集中在上半年,特別是6月,約佔到期總額的70%。這些債務的到期將對市場流動性和利率造成壓力,因為政府需要進行再融資以應對這些到期的債務。In 2025, the United States will face a large amount of public debt maturing, with the total amount of national debt maturing expected to be approximately US$9.2 trillion. These maturing debts are mainly concentrated in the first half of the year, especially June, accounting for about 70% of the total amount maturing. The maturity of these debts will put pressure on market liquidity and interest rates as the government will need to refinance to meet these maturing debts.

具體來說,根據不同的報導,2025年到期的國債數量如下:Specifically, according to various reports, the number of Treasury bonds maturing in 2025 is as follows:

總額:約9.2兆美元 Total: Approximately $9.2 trillion

集中時間:大部分到期債務集中在2025年上半年,尤其是6月。Concentrated time: Most of the maturing debts are concentrated in the first half of 2025, especially in June.

具體時間點:雖然具體的到期日期因債券類型而異,但整體而言,這些到期的債務將對美國政府的財政狀況造成壓力,尤其是在高利率環境下,政府需要發行新債來償還到期的債務。Specific timing: Although the specific maturity dates vary by bond type, overall these maturing debts will put pressure on the U.S. government's fiscal position, especially in a high-interest environment, when the government needs to issue new bonds to repay maturing debts.

萬一發生到期美公債到期沒有足夠買方,這時候必須發生聯儲量化寬鬆(QE)。In the event that there are not enough buyers for maturing U.S. Treasury bonds, the Federal Reserve will have to carry out quantitative easing (QE).

在量化寬鬆(QE)期間,美國聯邦儲備系統(Fed)主要購買了以下幾類金融資產:During quantitative easing (QE), the U.S. Federal Reserve System (Fed) mainly purchased the following types of financial assets:

1. 主要購買的金融資產Major financial assets purchased

國債(Treasury Securities):聯儲在QE期間大量購買美國國債,以降低長期利率並促進經濟增長。這些國債包括短期和長期的各類債券。The Fed purchased large amounts of U.S. Treasury bonds during QE in order to lower long-term interest rates and promote economic growth. These government bonds include both short-term and long-term bonds.

抵押擔保證券(Mortgage-Backed Securities, MBS):聯儲還購買了大量的抵押擔保證券,這些證券是由房貸組合而成的,旨在支持住房市場並促進信貸流動性。這些購買行為在2008年金融危機後尤為顯著,聯儲的MBS持有量在高峰時期達到約2.7兆美元。The Fed also purchased large amounts of mortgage-backed securities, which are bundles of mortgage loans, in an effort to support the housing market and facilitate the flow of credit. These purchases were particularly pronounced after the 2008 financial crisis, with the Fed's MBS holdings reaching about $2.7 trillion at their peak.

其他金融資產:在某些QE階段,聯儲也可能購買其他類型的資產,如公司債券等,以進一步支持金融市場的流動性。During certain QE phases, the Fed may also purchase other types of assets, such as corporate bonds, to further support liquidity in financial markets.

2. 聯儲的股東成份The Fed's shareholders

聯儲的股東主要是美國的商業銀行。具體來說:The Fed's shareholders are mainly U.S. commercial banks. Specifically:

總結來說,聯儲在QE期間的主要購買對象是國債和抵押擔保證券,而其股東主要是美國的商業銀行,這些銀行在聯儲的運作中扮演著特定的角色。In summary, the Fed's main purchases during QE are Treasury bonds and mortgage-backed securities, and its shareholders are mainly US commercial banks, which play a specific role in the Fed's operations.

目前聯儲財報,若聯儲QE對資產負債表的影響細節The current Fed financial report, if the Fed's QE has any details on the impact on the balance sheet

「海湖莊園協議」這個名稱,取自川普在佛州的私人度假勝地海湖莊園(Mar-a-Lago),其概念參照1985年美國與德、日、英、法簽署的「廣場協議」(Plaza Accord),當時各國協助貶值美元,促進美國經濟復甦。這項「協議」的構想,是由川普政府經濟顧問委員會主席米蘭(Miran)在去年一篇文章中提出的,當時他列舉了多種選項。如今,他已被任命為白宮經濟顧問委員會主席。The name "Mar-a-Lago Agreement" is taken from Trump's private resort Mar-a-Lago in Florida. Its concept refers to the "Plaza Accord" signed by the United States, Germany, Japan, Britain and France in 1985. At that time, these countries helped devalue the US dollar and promote the recovery of the US economy. The idea of this "deal" was proposed by Miran, chairman of the Trump administration's Council of Economic Advisers, in an article last year, when he listed a variety of options. He has now been appointed chairman of the White House Council of Economic Advisers.

米蘭在文章中指出,美國龐大貿易逆差的原因是美元被高估,「這種高估使得美國出口缺乏競爭力,進口變得便宜,進而削弱美國製造業的實力。」他表示,如今像中國與歐洲這樣的重要經濟體,可能不太願意加入新的協議,但關稅可以成為有效的施壓手段。Milan pointed out in the article that the reason for the huge U.S. trade deficit is the overvaluation of the dollar. "This overvaluation makes U.S. exports noncompetitive and imports cheap, thereby weakening the strength of the U.S. manufacturing industry." He said that important economies such as China and Europe may be reluctant to join new agreements, but tariffs can be an effective means of pressure.

從Ray Dalio的觀點來看,米蘭提出的海湖莊園協議涉及多個重要的經濟議題,包括關稅政策、友邦關係、美國出口產品的競爭力、美元的霸權影響以及全球貿易的衝擊。From Ray Dalio's point of view, the Mar-a-Lago agreement proposed by Milan involves several important economic issues, including tariff policies, relations with friendly countries, the competitiveness of US export products, the hegemonic influence of the US dollar, and the impact on global trade.

關稅政策 Tariff Policy

米蘭博士的海湖莊園協議中,關稅政策被視為重塑美國貿易體系的核心工具之一。根據報導,米蘭認為美國的貿易逆差問題與美元被高估有關,這導致進口商品便宜而出口商品昂貴,進而影響美國的製造業和經濟結構。Dalio也指出,關稅的使用可能是為了減少對外國生產的依賴,這在當前的全球經濟環境中尤為重要。但等於是美國主動離開全球自由貿易形成高關稅保護國家,其他國家仍在全球自由貿易,將造成國際化的美商分成國際分公司、美國本土公司獨立營運,美國的農產品、能源、原物料出口至其他沒有對美國報復關稅國家將增加,美國進口商品漲價,也無法增加美國工業產品競爭力。In Dr. Milan’s Mar-a-Lago agreement, tariff policy is seen as one of the core tools for reshaping the U.S. trade system. According to reports, Milan believes that the US trade deficit problem is related to the overvalued dollar, which makes imported goods cheap and exported goods expensive, thus affecting the US manufacturing industry and economic structure. Dalio also noted that the use of tariffs could be an effort to reduce reliance on foreign production, which is particularly important in the current global economic environment. But this is equivalent to the United States voluntarily leaving global free trade and becoming a country with high tariff protection, while other countries are still engaged in global free trade. This will cause internationalized American companies to be divided into international branches and American domestic companies to operate independently. The export of American agricultural products, energy, and raw materials to other countries that do not impose retaliatory tariffs on the United States will increase, and the prices of American imported goods will increase, which will not increase the competitiveness of American industrial products.

友邦關係 Friendly Countries relations

海湖莊園協議的實施可能會對美國的友邦關係產生影響。Dalio 提到,當美國推行保護主義政策時,可能會導致與主要貿易夥伴的緊張關係,這不僅影響經濟合作,也可能引發更廣泛的地緣政治衝突。這種情況下,友邦國家可能會對美國的貿易政策感到不安,進而影響雙邊貿易的穩定性。The implementation of the Mar-a-Lago agreement may have an impact on America’s relations with friendly countries. Dalio mentioned that when the United States pursues protectionist policies, it may cause tensions with major trading partners, which will not only affect economic cooperation but may also trigger broader geopolitical conflicts. In this case, friendly countries may feel uneasy about the US trade policy, which in turn affects the stability of bilateral trade.

美國出口產品競爭力

米蘭博士的報告強調,美元的高估使得美國的出口產品在國際市場上失去競爭力。Dalio 認為,這種情況如果不加以改善,將會進一步削弱美國的經濟基礎,特別是在製造業方面。米蘭提出的解決方案之一是促使美元貶值,以提高美國出口產品的價格競爭力,這一點與 Dalio 的觀點相呼應。Dalio 觀點,美國競爭力必須從基礎去努力:Dr. Milan's report emphasized that the overvaluation of the dollar has made US exports uncompetitive in the international market. Dalio believes that if this situation is not improved, it will further weaken the economic foundation of the United States, especially in the manufacturing sector. One of the solutions Milan proposed was to weaken the dollar to make U.S. exports more price competitive, a point echoed by Dalio. Dalio believes that the US must work on its fundamentals to improve its competitiveness:

產品創新 Product Innovation

生產力提升 Productivity Improvement

投資環境改善 Improved investment environment

拉高美國關稅,無法提高美國競爭力 Raising US tariffs will not improve US competitiveness

美元霸權影響The impact of US dollar hegemony

海湖莊園協議的另一個重要方面是美元的霸權地位。米蘭博士認為,美元作為全球主要儲備貨幣的地位使其被高估,這對美國經濟造成了長期的負擔。Dalio也指出,美元的強勢可能會導致其他國家尋求替代貨幣,這將對全球金融體系造成深遠影響。這種情況下,美國需要重新評估其貨幣政策,以維持美元的全球地位。關稅拉高、配合弱勢美元,可能造成美元國債投資人疑慮,升高美國國債殖利率降低美國國債安全性。Another important aspect of the Mar-a-Lago agreement is the hegemony of the U.S. dollar. Dr. Milan believes that the dollar's status as the world's main reserve currency makes it overvalued, which poses a long-term burden on the US economy. Dalio also pointed out that the strength of the U.S. dollar could lead other countries to seek alternative currencies, which would have far-reaching implications for the global financial system. In this situation, the United States needs to reassess its monetary policy to maintain the global status of the dollar. Higher tariffs, coupled with a weaker dollar, could cause concerns among U.S. Treasury investors, raising U.S. Treasury yields and reducing the security of U.S. Treasury bonds.

中國在全球貿易中的地位影響 The impact of China's position in global trade

米蘭博士的報告中提到,美元的高估使得美國的出口產品在國際市場上失去競爭力。Dalio認為,這種情況如果不加以改善,將會進一步削弱美國的經濟基礎,特別是在製造業方面。他指出,中國在全球貿易中的地位不斷上升,這使得美國必須重新評估其貿易政策,以維持競爭力。Dalio建議,應該考慮讓人民幣對美元升值,這可以通過中國出售美元資產來實現,並同時刺激內需,這樣的策略將有助於改善中美之間的經濟不平衡。中國影響:Milan's report mentioned that the overvaluation of the US dollar has made US exports noncompetitive in the international market. Dalio believes that if this situation is not improved, it will further weaken the economic foundation of the United States, especially in the manufacturing sector. He noted that China's growing role in global trade requires the United States to reassess its trade policies to remain competitive. Dalio suggested that consideration should be given to allowing the RMB to appreciate against the U.S. dollar, which could be achieved by China selling its U.S. dollar assets and stimulating domestic demand at the same time. Such a strategy would help improve the economic imbalance between China and the United States. Chinese influence:

中國仍在全球貿易中的地位持續上升,關稅戰只是一個小修正。

美國與中國貿易脫鉤。

全球貿易衝擊 Global trade shock

最後,海湖莊園協議的實施可能會對全球貿易格局造成重大衝擊。Dalio警告,當前的貿易政策不確定性加劇了市場的波動,並可能導致全球經濟的動盪。米蘭的報告中提到的各種政策選項,如發行百年期債券和建立主權財富基金,都是為了應對這些挑戰,但其實施的可行性和效果仍然存在爭議。Finally, the implementation of the Mar-a-Lago agreement could have a significant impact on the global trade landscape. Dalio warned that current trade policy uncertainty has increased market volatility and could lead to turmoil in the global economy. The various policy options mentioned in the Milan report, such as issuing 100-year bonds and establishing sovereign wealth funds, are intended to address these challenges, but their feasibility and effectiveness remain controversial.

總結來說,從Ray Dalio的觀點看,米蘭博士的海湖莊園協議提出了一系列旨在重塑美國經濟和貿易政策的措施,這些措施的成功與否將直接影響美國的經濟競爭力及其在全球貿易中的地位。In summary, from Ray Dalio’s point of view, Dr. Milan’s Mar-a-Lago Agreement proposes a series of measures aimed at reshaping the US economic and trade policies. The success or failure of these measures will directly affect the US economic competitiveness and its position in global trade.

綜合分析

「海湖莊園協議」只集中關稅、美元弱勢、延長低息國債,會讓全球投資人對美債信心下降,更讓全球投資人認為是美國競爭力下降,測試這樣新關稅、貨幣制度要很小心,不小心會造成美債殖利率爆升,發生金融風暴及經濟蕭條。The "Mar-a-Lago Agreement" only focuses on tariffs, a weak dollar, and the extension of low-interest Treasury bonds. It will reduce global investors' confidence in U.S. debt and make global investors believe that the United States' competitiveness has declined. We must be very careful when testing such new tariffs and monetary systems, as we may accidentally cause a surge in U.S. Treasury yields and a financial crisis and recession.